Family Cottage Planning

As cottage season gradually approaches a close, it’s a great time to talk about capital gains, taxation and financial planning for homeowners who also own a cottage property.

We never like to think of the worst coming to pass, but if you own a cottage, it’s a good idea to sit down for a family meeting and decide what will happen to this property in the future. Whether you would like to think ahead to a succession plan, or you simply know that you wish to sell your cottage at a later date, it’s good to understand and plan for the tax implications that lie ahead.

In this Special Issue brought to you by our head of taxation Laura Schmidt, we’d like to break down a few tax concepts that pertain to cottage properties, and explain some of the main options clients should consider when planning for the future.

Will I be taxed with capital gains when I sell? What about the Principal Residence Exemption?

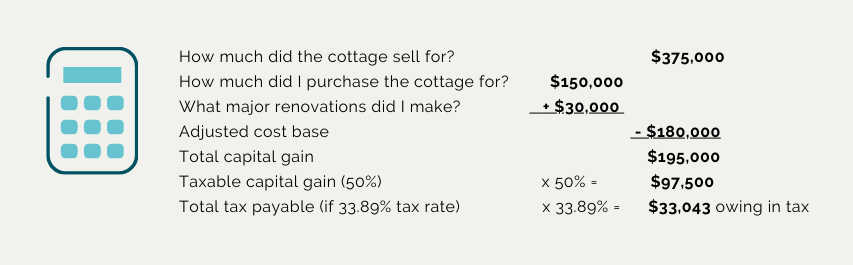

According to CRA, when a property changes ownership for any reason, such as sale or death, it is a disposition and triggers tax considerations. Upon disposition, cottages are taxed like any other capital asset and are subject to capital gains. The amount of the capital gain is equal to the fair market value (FMV) of the cottage at the time of sale MINUS the adjusted cost base (ACB) of the property. The ACB includes the purchase price, PLUS any major renovations or work done for the betterment of the property but does not include costs for regular maintenance and repair. Under the current iteration of the Income Tax Act, 50% of this capital gain is taxable and will be included as income on your personal tax return in the year of sale.

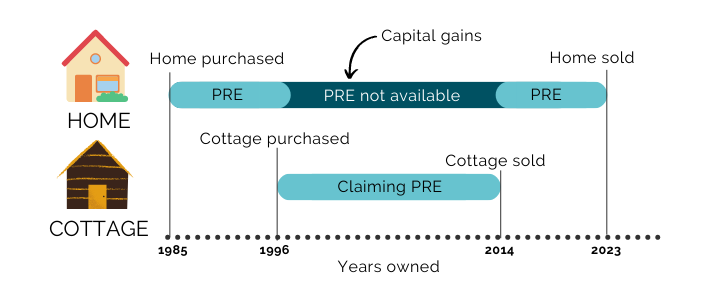

That said, the Principal Residence Exemption (PRE) is an exemption that reduces the capital gain and tax payable on the disposition of a property, on a per year basis, if that property was a taxpayer’s primary residence during any or all years it was owned.

Most people don’t live in their cottages year-round, but Canadian tax law specifies that as long as the cottage was occupied at some time during the year (with no minimum time requirement) it may be considered for the PRE. The catch is that the PRE may only be claimed on one property per year and only once by the family unit (i.e. spouses who share a home or cottage). This restriction means that you may only claim the PRE for either your home or your cottage in any given year, but not both. This determination only needs made at the time of sale, but it’s helpful to think about it and talk with your family about the intentions for all properties currently owned as a family unit.

At Innova, we strive to have our clients be as informed as possible about the financial impact of family decisions such as these. As such, our planning process accounts for all your intentions and properties to determine the most optimal designation for the largest exemption and minimum tax payable. For example, it may be tempting to want to claim the PRE on the sale of your cottage for all of the years you’ve owned it, but what about the tax implications of giving up the PRE for those years if you were to sell your home or other qualifying primary residence at some point in the future?

What if I want the cottage to stay in the family?

Many families wish to keep their cottage property available for future generations, and there are several different planning methods to accomplish this. It is crucial to have this discussion with family members – especially if you have the intention for the cottage to pass to more than one person – to determine who will have a right to cottage use and when, who will perform the maintenance and pay the associated costs, who gets final say on development of the property, what are the conditions for a potential future sale, what happens in the case of a dispute, and what are the tax consequences of any decisions made.

If there are to be multiple owners, a co-ownership agreement should be considered.

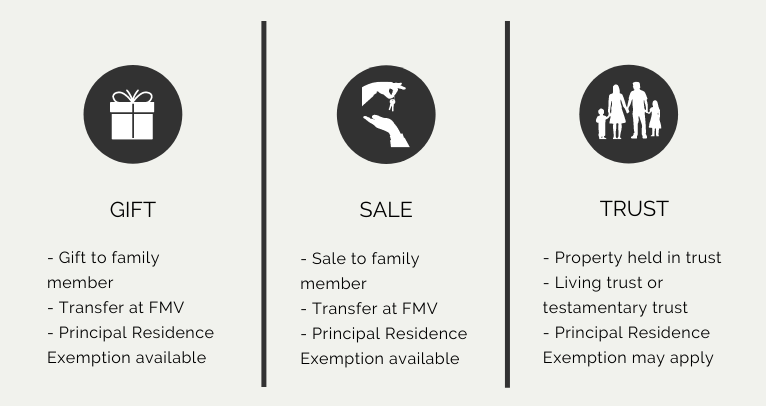

If the cottage is owned by spouses and one passes away, there will be a rollover to the surviving spouse with no immediate tax consequences. However, what happens with the cottage after that is important. If the cottage is to be transferred to one or more children, joint ownership with rights of survivorship (JTWROS) may not be the best option. Here, we break down three better ways of accomplishing this disposition: by gift, sale, or trust.

Gift

When a cottage is gifted to a family member(s), the transferor is deemed to have sold the property at fair market value and thus will report a capital gain on their taxes. The recipient(s) will acquire the cottage at fair market value, which becomes their cost base. In the case of a gift, the Principal Residence Exemption is available to claim against the transferor’s capital gain. Additionally, land transfer tax does not apply in this scenario.

Sale

Selling the cottage to family members is another method of keeping the cottage in the family, however, there is a major tax trap here and careful planning is required. If the property is sold at fair market value, there is no issue and the cottage will be treated in the same way as gifting; the transferor will pay tax on the capital gain on the property and the fair market value will become the purchaser’s new adjusted cost base. There are methods to accomplish this sale in a way that defers the payment on the proceeds, talk to your advisor about these options.

However, if the sale takes place at less than fair market value (which is tempting when selling to family members), double taxation will result. The duplication occurs in this case because the transferor will pay capital gains calculated at the fair market value and pay the same tax as above, but the purchaser’s adjusted cost base will be the price paid, not the FMV, which leaves them with a lower cost base that will be taxed again upon a disposition in the future.

The Principal Residence Exemption is available in the case of a sale to a family member, and land transfer tax does apply.

Trust

Another option is to have the cottage property held within a trust. Living (inter vivos) trusts encourage family discussion, help avoid probate tax and complex settlements, and can provide specific instructions for the property. Especially for blended families, a family trust can often be beneficial.

Trusts come with their own complexities too, however. There may be tax consequences on the transfer of the property into the trust, the trust requires a separate tax return (taxed at top rates), and there is a deemed disposition of assets within the trust every 21 years (with associated tax implications). With a few exceptions, this type of trust may also claim the Principal Residence Exemption if it is appropriate.

A testamentary trust may also be established upon death of the cottage owner. If spouses own the cottage together and one dies, the property may be held in a testamentary spousal trust for the surviving spouse. Upon the death of the second spouse, the cottage may then pass to one or more children as beneficiaries of the trust. This type of trust is taxed at graduated rates. However, a testamentary trust is not an eligible trust to claim the Principal Residence Exemption, meaning any gains within the trust would be fully taxable.

Are there any tax consequences to renting my cottage out?

There are always tax risks if you choose to rent out your cottage. CRA may decide that the cottage is now an ‘income-producing property’, meaning that it is no longer eligible for the Principal Residence Exemption unless you are able to meet certain criteria. You have to demonstrate that generating income is ancillary to the main use of the cottage, no depreciation was claimed on the cottage, and no structural changes were made to make it suitable for rental or business purposes.

With Airbnb and VRBO more popular than ever for short-term rentals, it is important to note that rental income is taxable and must be reported on your annual tax return (we can help with that!). All receipts on repairs, renovations, and other expenditures for the cottage must be tracked, and in some cases, specific insurance is required for your rental.

Discuss renting with your family and the intentions for your cottage.

If you have any questions, please reach out to us! There are a myriad of complexities when it comes to the taxation of cottage properties, and many of these topics – such as US cottage properties, the capital gains reserve, and probate tax – are beyond the scope of this newsletter. I am always happy to work with cottage owners to analyze your whole real estate portfolio and determine the best options to optimize taxes and minimize capital gains.

We thank you for your continued trust in our management and remain available to you as needed.

Further Reading

Estate Planning – Don’t take these shortcuts

https://www.advisor.ca/tax/estate-planning/dont-take-these-shortcuts/

Tax Planning Strategies for Cottage Owners

https://www.bdo.ca/en-ca/insights/tax/tax-articles/tax-planning-strategies-cottage-owners/

How to hand down your cottage while keeping the peace and saving money

https://cottagelife.com/realestate/how-to-hand-down-your-cottage-while-keeping-the-peace-and-saving-money/

Disclaimer:

Aligned Capital Partners Inc.(ACPI) is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). Investment products are provided through ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Please contact Jean-François Démoré or Cliff Richardson, or visit https://invest.innovawealth.ca for additional information about the Innova Tactical Asset Fund. All non-securities related business conducted by Innova Wealth Partners is not as agent of ACPI. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Jean-François Démoré or Cliff Richardson.

Information has been compiled from sources believed to be reliable. All opinions expressed are as of the date of this publication and are subject to change without notice. Content is prepared for general circulation and has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The information contained does not constitute an offer or solicitation to buy or sell any investment fund, security or other product or service. Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI. For current performance information, please contact Innova Wealth Management of Aligned Capital Partners Inc. Important information about the Fund is contained in the offering memorandum which should be read carefully before investing.

- Hits: 12171