Issue #66 - Cash is King!

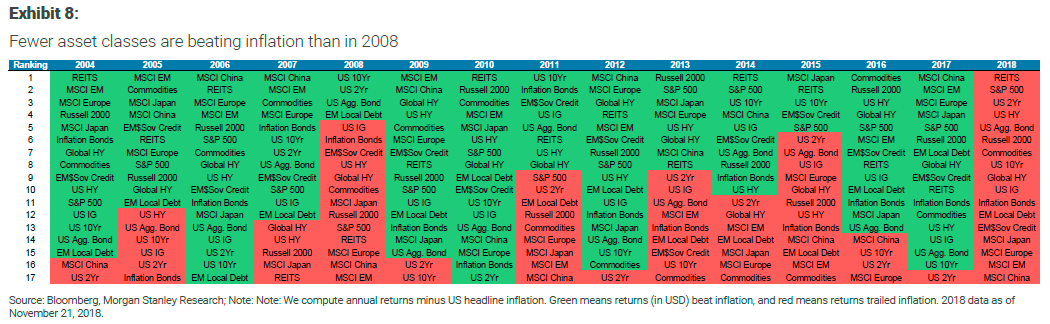

From January 1st to November 21st, 2018, not a single one of the major investment asset classes has beaten inflation, and this statement was uttered before this week’s blood bath in tech stocks. By many measures, 2018 has been as bad of a year as 2008, just not quite as drastic.

The chart below highlights investments that have outperformed inflation in green and those that have trailed in red for every year since 2004. As you can see, not a single asset class has managed this feat thus far in 2018 whereas there were at least four places to hide in 2008, predominantly in US bonds.

But with interest rates rising, those bonds have also languished in the red this year. Despite interest rates increasing at a slower pace in Canada, both Canadian government and corporate bonds also suffered the same fate.

This trend leaves two asset classes that have made money so far this year, neither of which is listed on the chart above:

1- Cash (High Interest Savings, etc.)

2- Alternative Investments

As you are all aware, we have been recommending significant cash positions in all portfolios to provide some shelter from markets just like these. We have also been adding alternative investments such as option writing strategies and long-short hedge funds for the past two years.

We have been discussing these types of positions for some time and will continue to recommend them to you where appropriate.

What is causing these markets?

Firstly, markets have historically been this volatile and only in the past few years has this volatility not been the norm. We wrote about the ‘complacency issue’ we have been seeing on the markets since March 2017 (IMI#47 – The Return of Irrational Exuberance) which has caused these unusually calm markets.

That being said, there are a few factors that are contributing to this recent volatility:

1- The famous ‘8th Inning’

Economic growth cycles typically last between 6 and 8 years, with only a select few reaching double-digits. The recovery from the ‘Great Recession’ will be entering its tenth year in March 2019 and many see this milestone as the 8th Inning of the market cycle. Not quite the end, but almost game over.

The stock market is a forward looking indicator which tries to forecast where the economy will be in the next 6 to 12 months, so it’s clear that the markets are signalling that the ‘good times’ may be coming to end.

For this reason, investors are changing their portfolios and moving away from ‘growth’ stocks (Tech) toward more conventionally ‘safe’ stocks like utilities, real estate, and healthcare. This move has led to a blood bath on the technology heavy Nasdaq which has suffered three 5% drop days in the last 30. This drop has seeped over into the broader S&P500 market given that many large tech stocks now comprise a much larger portion of that index. We warned about this risk extensively and how market priced ETFs would ultimately bear the brunt of the damage of a correction in “IMI#53 – The High Price of Low Cost Investing” and have done our best to stay away from stocks that are heavily covered, and thus exposed to these types of stocks.

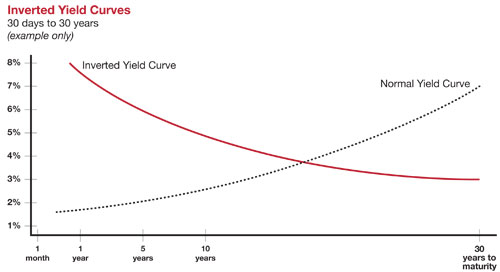

2- The Inversion of the Yield Curve

Known by many as the best forecaster of a coming recession, the inversion of the yield curve is the canary in the coal mine of economic forecasting. It occurs when long-term interest rates (the cost for government to borrow money for 15 years or more) drop below short-term interest rates. To put this in layman’s terms, as 1 year mortgage interest rates become higher than 5 year mortgage rates.

The last inverted yield curve to occur lasted until the summer of 2007: 6 to 12 months before the trouble started… Without going into too much detail, you could see why having it almost happen again this week is frightening to some investors.

There is a great blog by an actual financial pundit which explains this phenomenon in great detail and can be accessed here for those that are curious: https://www.iwillteachyoutoberich.com/blog/inverted-yield-curve/ From that article, an actual financial pundit’s reaction to an inverted yield curve:

3- China

As the second largest economy in the world continues to undergo substantial economic changes, there is bound to be some hiccups along the way. China is moving from the t-shirt manufacturer of the world to the hot spot for all things technology hardware, both design and manufacturing. Clearly, they are making a move up the value scale. China is now home to more PhDs than any other country in the world and the government is directly infusing money into tech, science, mathematics, and engineering industries.

With that massive change underway, the economy is slowing and now only growing at 6% (approximately three times faster than the Canadian economy). Nonetheless, as the primary driver of growth around the world for the past 10 years, its economic slowdown has sent shockwaves around the world.

Adding fuel to this fire is the ongoing trade war with the US. Good news has been hard to come by and few believe what comes out of President Trump’s twitter feed, so pessimism toward Chinese stocks is rampant on international markets.

How does this impact you?

Fortunately, we have been discussing this coming correction with each and every one of you, and so seeing some red on the markets should come as no surprise. We recommended excess cash in your portfolios that should allow us to ‘buy’ during the down markets, as well as option writing strategies to generate income through the drops to client's for whom this strategy was appropriate. That being said, no portfolio is immune to all crashes but we expect our recommendations to maintain an average 50% downmarket capture, thus reducing the damage caused by the markets.

Where do we go from here?

We would love to tell you that sunshine and rainbows are just around the corner, but in the wise words of BTO “You ain’t seen nothing yet”. Although October’s 6% drop on the Toronto Stock Exchange rattled some nerves, it is important to remember that a full stock market crash sees those kinds of losses on a daily basis. In fact, the Toronto Stock Exchange lost 23% of its value the WEEK of October 10th, 2008.

Although we have been recommending that clients lower their portfolio risk in the face of what we expect to be harsh markets, all investors will be feeling the damage given that almost nothing is making money right now. It is in times like these that we are thankful for our defense first mentality and the significant cash positions we have built up.

We do not expect the markets to enter a sustained bull market in the near term and so we will not be recommending deploying cash in the near term until we see at least another 10% drop in the overall markets.

In other words, the going’s about to get tough so having confidence in your investment strategy over the next few months will be imperative. If you find yourself growing concerned, please reach out so that we may discuss this strategy in detail to make sure you are still on the right path to meet your long-term goals, as it can be hard to see the forest from the trees, especially when the trees are on fire…

As always, we are here to help - so don't hesitate to call or email.

Innova Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI). Jean-François Démoré, as an agent of Innova Wealth Management/ACPI is registered to provide investment advice in the provinces of Ontario, Quebec, and British Columbia. Investment products are provided by ACPI, a member of the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and the Canadian Investor Protection Fund (www.cipf.ca). All non-securities related business conducted by J-F Demore as a representative of Innova Wealth Builders is not covered by the Canadian Investor Protection Fund and is not under the supervision of ACPI.

The information contained herein was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell any securities mentioned. The views expressed are those of the author and not necessarily those of ACPI.

- Hits: 7283