INWP Lender Spotlight: May 2026

Northern Ontario Housing & Mortgage Monthly

For clients in North Bay, Greater Sudbury, Muskoka, Sault Ste. Marie & Timmins — May 2026

Market Positioning Summary - May 2026

Northern Ontario housing markets continued to move toward more balanced conditions through April.

Sales activity has softened across most regions, not due to a lack of demand, but because affordability and financing constraints are limiting what buyers can do. At the same time, inventory is building, giving buyers more choice and extending time on market.

The Bank of Canada held its policy rate steady again, reinforcing a more stable rate environment. That stability is helping sentiment, but borrowing costs remain high enough to keep buyers cautious.

Rental fundamentals remain strong and continue to support investor demand, particularly in smaller multi-unit properties.

Interest Rates and Forward Outlook

The Bank of Canada held its overnight rate at 2.25 percent, with no change at its most recent meeting.

Overnight Rate: 2.25%

Prime Rate: Approximately 4.45%

5-Year Government of Canada Yield: Approximately 3.00 to 3.20%

5-Year Fixed Mortgage Rates: Approximately 4.30 to 4.90%

We are now in a rate stability phase rather than a tightening cycle.

The key issue for the market is not whether rates are rising. It is that they remain high enough to limit borrowing capacity.

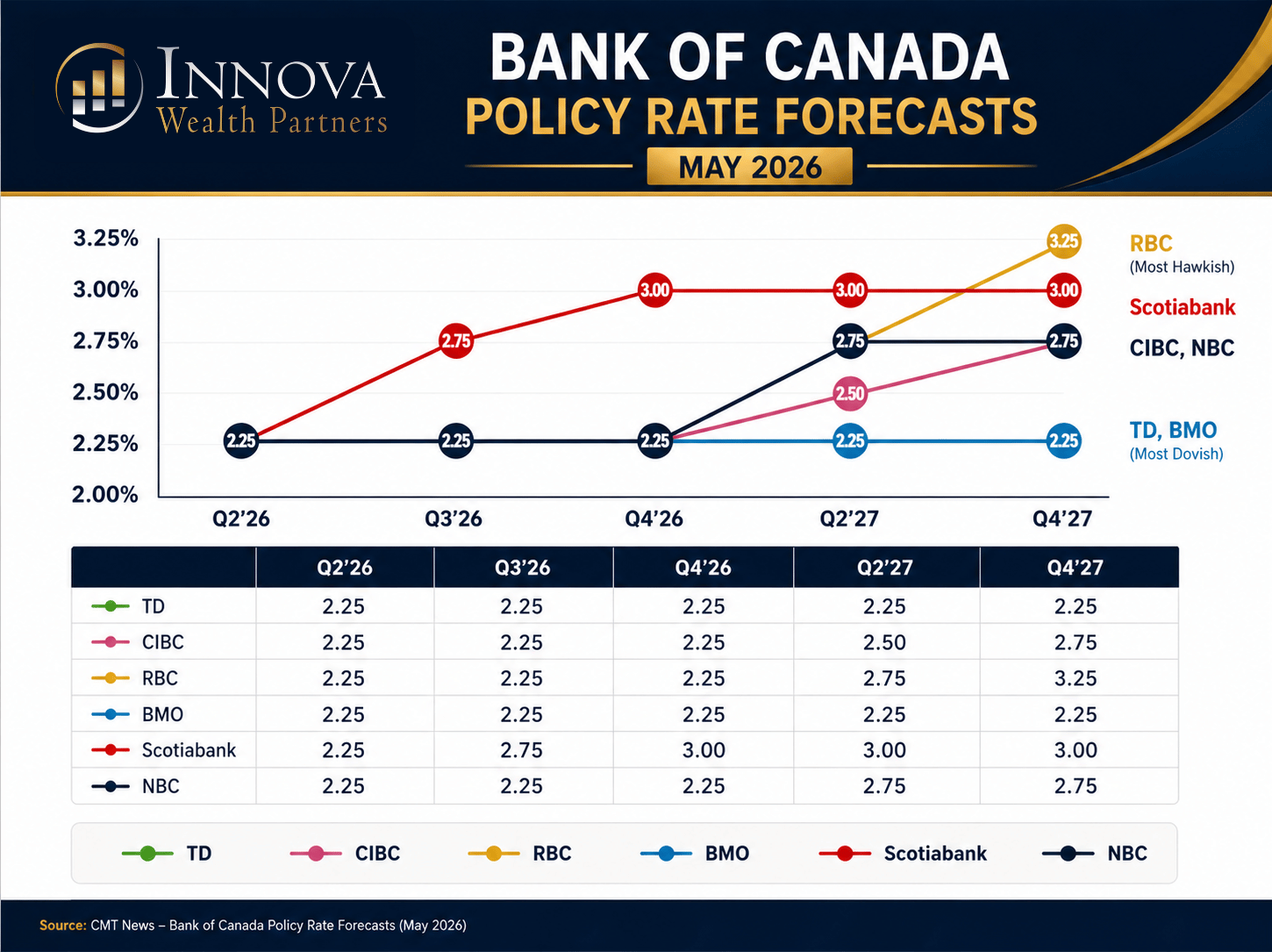

Bank Economics Policy Rate Outlook

Forecasts from the major banks (RBC, Scotiabank, CIBC, BMO, TD, National Bank) show a consistent near-term outlook, with more variation further out.

2026 Outlook

- Most banks expect little movement through 2026.

- Policy rates are expected to remain in a range of approximately 2.25 to 3.00%.

- Scotiabank is more aggressive toward the higher end of that range.

- TD and BMO are more conservative and remain closer to current levels.

2027 Outlook

Forecasts begin to spread:

- RBC: Approximately 3.25%

- CIBC and National Bank: Approximately 2.75%

- TD and BMO: Approximately 2.25%

Key takeaway: there is no clear expectation of rapid rate cuts. The base case is gradual normalization.

What This Means for Real Estate

Borrowing costs remain restrictive enough to slow demand.

Fixed rates may ease modestly but not significantly in the near term.

Variable or adjustable rate relief is less likely.

Uncertainty around timing continues to keep buyers cautious and selective.

Market Trends

Across Northern Ontario:

Sales are flat to down year over year

Listings are increasing

Days on market are rising

Pricing is holding, but less forgiving

This is no longer a supply-driven market. Pricing and execution matter again.

North Bay Market Snapshot

Sales were down approximately 8 to 12% year over year, with a modest seasonal lift from March.

Sales to New Listings Ratio: Approximately 45 to 50%

Days on Market: 32 to 45

Months of Inventory: Approximately 4.5 to 5.5

Entry-level homes continue to move. Mid-range properties are slower. Higher-end listings require sharper pricing.

Takeaway: demand is still present, but buyers are selective.

Sudbury Market Snapshot

Sales are roughly flat year over year, but inventory is building faster than absorption.

Sales to New Listings Ratio: Approximately 40 to 45%

Days on Market: 35 to 50

Months of Inventory: Approximately 5.0 to 6.0

Entry-level remains stable. Mid-range is slowing. Multi-unit demand remains supported.

Takeaway: stable on the surface, but gradually loosening.

Timmins Market Snapshot

Timmins remains the strongest market in the region.

Sales: Up approximately 5 to 10% year over year

Sales to New Listings Ratio: Approximately 55 to 60%

Days on Market: 20 to 30

Months of Inventory: Approximately 3.5 to 4.5

Takeaway: tight and liquid market supported by investor demand.

Sault Ste. Marie Market Snapshot

Sales declined approximately 10 to 15 percent year over year, with rising inventory.

Sales to New Listings Ratio: Approximately 35 to 40%

Days on Market: 40 to 55

Months of Inventory: Approximately 5.5 to 6.5

Takeaway: shifting toward buyers, with early pricing pressure emerging.

Muskoka Market Snapshot

Sales are down approximately 20 to 30% year over year.

Sales to New Listings Ratio: Approximately 30 to 35%

Days on Market: 60 or more

Months of Inventory: 7 or more

Takeaway: still in a correction phase, particularly in discretionary segments.

Rental Market

Data from Canada Mortgage and Housing Corporation continues to show tight conditions.

Vacancy rates are approximately 1.5 to 3%

Rent growth is approximately 4 to 7%

Limited new supply continues to support strong rental fundamentals.

Implication: cash flow remains the foundation of investor demand.

Lending Environment

Qualification remains tight

Rental income scrutiny is increasing

The stress test remains a constraint

Trends include more use of 30-year amortizations and increased use of alternative or private lending.

Investor focus has shifted toward cash flow, debt service coverage, and conservative underwriting.

Outlook Next 3 to 6 Months

Base Case

Rates hold, activity gradually improves, markets remain balanced.

Bull Case

Earlier rate cuts drive stronger demand and tighter inventory.

Bear Case

Rates remain elevated longer, leading to continued softness in demand.

Strategic Takeaways

Buyers

You have more negotiating power. Focus on structure and long-term affordability.

Investors

Cash flow and realistic underwriting are critical. Avoid thin-margin deals.

Sellers

Pricing matters again. Expect longer timelines and more conditions.

Bottom Line

This is a fundamentals-driven market.

Financing costs, pricing discipline, and execution are what separate good outcomes from missed opportunities.

Sources

Bank of Canada

Canadian Real Estate Association

North Bay and Area REALTORS Association

Sudbury Real Estate Board

Canada Mortgage and Housing Corporation

CMT Bank Economics May 2026

If you want a personalized renewal, purchase, or investment analysis, just email

Thanks for reading!

Caleb O'Connor, CFP

Partner | Financial Planner | Mortgage & Lending Lead, Innova Wealth Partners

Mortgage Agent Level 1, HomeLink Financial Corp, Brokerage Lic. #10875

📩

This publication is for informational purposes only and shall not be construed to constitute any form of advice. The views expressed are those of the author alone. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

- Hits: 1802