Issue #54b - New Mortgage Rules

How the new mortgage rules will affect you

In an effort to slow down the ever expanding real estate bubble in Canada’s largest markets, the Office of the Superintendent of Financial Institutions (OSFI), Canada’s banking regulator, has released a new set of mortgage rules intended to make it harder for Canadians to refinance mortgages. This change could impact you in the following ways:

What is Changing?

All borrowers will have to pass a financial stress-test to determine if their ability to withstand rising interest rates on their new mortgage. The stress-test is designed to ensure that mortgagors can still afford to pay their mortgage should rates increase 2% higher than current rates. In other words, if you can’t afford your mortgage at 4.89% (current market mortgage rate plus 2%), then you won’t qualify for a mortgage under the new guidelines.

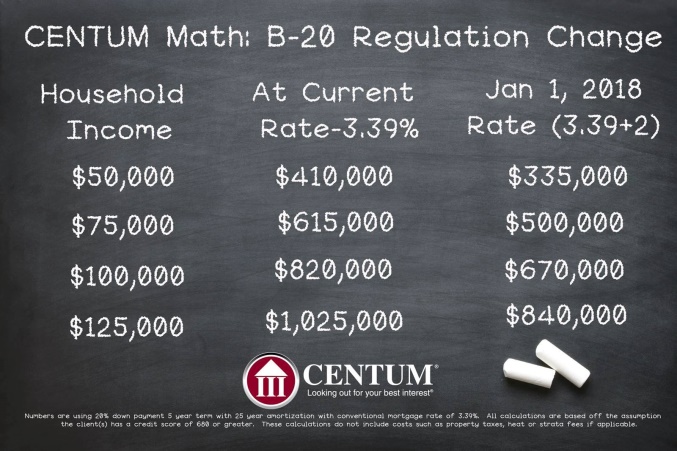

What is the Impact?

The following chart shows the impact on borrowers of different income levels:

As you can see, a borrower with an income of $100,000 per year with a 20% down-payment on a home has seen their purchasing power reduced by $150,000.

How does this affect You?

According to TD Economics, this new regulation is expected to drag down real estate prices 2% to 4% in 2018. Royal Lepage CEO expects that 905 area code communities will be hit the hardest, given that they saw the largest year-over-year gains between 2015 and 2017 and are more popular with young families looking to ‘upsize’ their home.

If you are nearing retirement and are considering a significant refinance or the purchase of a second property, it might be wise to secure a commitment before Dec 31st. Mortgages renewing from now until March 15th are eligible for refinancing under the old rules, as long as they are submitted before year-end.

How Will Rates be Impacted?

Likely, this regulation will mean a slowing of the rapid increases we have seen on mortgage rates over the past 3 months. Combined with the recent rate hikes by the Bank of Canada, this should have the desired dampening effect on the housing market. Given the slowing Canadian economy and serious concerns over the on-going NAFTA negotiations, it seems unlikely that Mr. Poloz, the governor of the Bank of Canada, will increase rates further before these rules come into effect. More likely, these new mortgage rules may translate into a glut of new borrowers during the spring of 2018 which may force lenders to cut rates in order to keep their market shares.

How Innova Wealth Builders Can Help!

Innova clients benefit from an in-house mortgage broker who monitors the mortgage market for rate sales and competitive offerings. 120 days prior to your renewal, Tanya can help you lock-in a rate to protect you against future rate increases. Locking-in a rate does not commit you to anything but secures a good rate for you while allowing you to continue to shop the market.

As always we are here to help, so please don’t hesitate to call or email!

Innova Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI). Jean-François Démoré, as an agent of Innova Wealth Management/ACPI is registered to provide investment advice in the provinces of Ontario, Quebec, and British Columbia. Investment products are provided by ACPI, a member of the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and the Canadian Investor Protection Fund (www.cipf.ca). All non-securities related business conducted by J-F Demore as a representative of Innova Wealth Builders is not covered by the Canadian Investor Protection Fund and is not under the supervision of ACPI.

The information contained herein was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell any securities mentioned. The views expressed are those of the author and not necessarily those of ACPI.

- Hits: 6479